Loan Calculator For Commercial Property

Loan Calculator For Commercial Property

Inna Radford | 1st August 2024 |

Commercial Real Estate Calculator

Results:

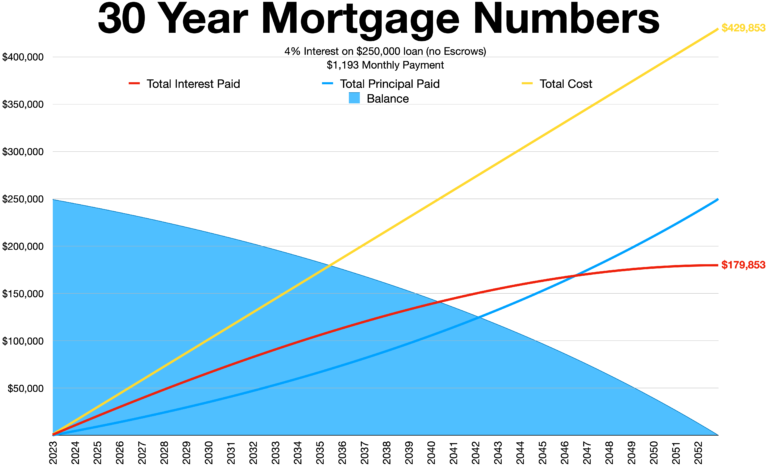

What Is A Loan Calculator For A Commerical Property?

A commercial loan property calculator is an essential tool for anyone considering a commercial mortgage.

It helps estimate monthly payments, total interest, and overall costs associated with a commercial loan.

H2

Are You Looking For Commercial Property?

Let us find a property that matches your exact requirements.

Commercial Real Estate Guide

Key Elements Of A Loan Calculator For A Commercial Property?

- Loan Amount: The total amount borrowed.

- Interest Rate: The annual interest rate of the loan.

- Loan term: The duation of the loan in years.

- Payment Frequency: Unually monthly

Amortization Period: The time over which the loan payments are calculated.

How To Use A Commercial Property Calculator

1. Input Loan Details: Enter the loan amount, interest rate, loan term, and amortization period.

2. Calculate Payments: The calculator will provide monthly payment amounts and a breakdown of the principal and interest.

3. Compare Scenarios: Adjust variables to see how changes in interest rates or loan terms affect payments.

Popular Banks And Their Interest Rates

Generally range from 4.5% to 6% depending on the loan term and property type

Typically between 4% and 5.5%.

Typically between 4% and 5.5%.

Vary from 4% to 6%.

Usually between 4.5% and 6%.

Generally from 4.5% to 6%.

Typically between 4% and 5.5%.

Vary, generally between 5% and 7% for alternative lending.

For short-term financing, rates can be between 4% and 7%.

What Is A Commercial Mortgage?

A commercial mortgage is a type of loan specifically designed for purchasing, refinancing, or improving commercial real estate. Unlike residential mortgages, which are used to buy homes or other residential properties, commercial mortgages are used for income-generating properties or business purposes.

Types Of Properties For A Commercial Mortgage

- Office Buildings: Spaces rented to businesses.

- Retail Properties: Stores, shopping centers.

- Industrial Properties: Warehouses, manufacturing facilities.

- Multifamily Properties: Apartment buildings, student housing.

What Are Commercial Loan Terms and Payment Structures?

Common Loan terms

- Loan-to-Value (LTV) Ratio: The ratio of the loan amount to the appraised value of the property. Typically ranges from 65% to 80%.

- Debt Service Coverage Ratio (DSCR): The ratio of net operating income (NOI) to annual debt service. A DSCR of 1.25 or higher is often required.

- Interest Rates: Can be fixed or variable. Fixed rates remain the same for the loan term, while variable rates can change based on market conditions.

- Amortization: The process of paying off the loan over time through regular payments. Amortization periods for commercial loans often range from 10 to 30 years.

Commercial Payment Structures

- Principal and Interest Payments: Monthly payments that cover both the loan principal and interest.

- Interest-Only Payments: Payments only cover interest, typically for a short period at the beginning of the loan term.

- Balloon Payments: A large payment due at the end of the loan term after making smaller, regular payments throughout the term.

Real Estate Contract Terms

Commercial Loan Repayment Example:

Scenario

- Loan Amount: $1,000,000

- Interest Rate: 5%

- Loan Term: 20 years

- Amortization Period: 25 years

Calculation

- Monthly Payment: Approximately $5,848

- Total Interest Paid Over 20 Years: Approximately $1,403,520

- Balloon Payment at End of Term: If the loan has a 20-year term but a 25-year amortization, a balloon payment of around $543,000 would be due at the end of the term.

What Is A Commercial Loan Balloon Payment?

A balloon payment is a lump sum payment due at the end of a loan term after a series of smaller, regular payments. This payment is significantly larger than the previous payments.

Advantages and Disadvantages

- Advantages: Lower monthly payments during the loan term, potential for lower interest rates.

- Disadvantages: Large payment due at the end, which can be a financial burden if not planned for.

Mitigation Strategies

- Refinancing: Obtain a new loan to cover the balloon payment.

- Sinking Fund: Set aside funds over time to cover the balloon payment.

Texas Commercial Lease Agreements

Commercial Property Interest Rates

Types Of Interest Rate

- Fixed Rates: Remain constant throughout the loan term, providing predictability.

- Variable Rates: Fluctuate with market conditions, potentially offering lower initial rates but with the risk of increase.

Factors Affecting Interest Rates

- Economic Conditions: Inflation, economic growth, and monetary policy.

- Creditworthiness: The borrower’s credit score and financial health.

- Loan Details: Loan amount, term, and property type.

Current Trends

As of 2024, commercial mortgage rates vary but typically range from 3.5% to 6.5%, depending on the factors mentioned above.

Types Of Commercial Loans

SBA Loans

- Description: Government-backed loans provided by the Small Business Administration (SBA).

- Types: SBA 7(a) for general purposes, SBA 504 for real estate and equipment.

- Benefits: Lower down payments, longer terms, lower interest rates.

- Eligibility: Business size standards, good credit history, ability to repay.

Hard Money Loans

- Description: Short-term loans secured by real estate, often used for property flips or renovations.

- Characteristics: Higher interest rates, shorter terms, easier to obtain.

- Risks: Higher cost, short repayment period.

Bridge Loans

- Description: Short-term financing used until permanent financing is obtained or an existing obligation is removed.

- Characteristics: Quick funding, higher interest rates, short terms (6 months to 3 years).

- Uses: To bridge gaps in financing, during property transitions.

Landlord Insurance In Texas

How Do I Qualify For A Commercial Loan?

Key Requirements

- Credit Score: A good business credit score (typically 650 or higher) is crucial.

- Business Financials: Strong financial statements, including profit and loss statements, balance sheets, and cash flow statements.

- Business Plan: Detailed plan outlining the business’s goals, market analysis, and financial projections.

- Collateral: Commercial property or other assets to secure the loan.

- Experience: Proven experience in the industry or business.

Business Credit Score And How To Improve It

Importance

- Loan Approval: A higher credit score improves chances of loan approval.

- Interest Rates: Better scores often result in lower interest rates.

How to Improve Your Business Credit Score

- Pay Bills on Time: Timely payments boost your score.

- Reduce Debt: Lowering outstanding debt improves your credit utilization ratio.

- Monitor Credit Reports: Regularly check for errors and dispute inaccuracies.

- Build Credit History: Establish and maintain a history of responsible credit use.

Real Estate Contract Terms

What Is A Lending Ratio In Business?

Loan-to-Value (LTV) Ratio

- Definition: The ratio of the loan amount to the appraised value of the property.

- Importance: Lower LTV ratios indicate less risk for lenders, often leading to better loan terms.

- Typical Ratios: Usually between 65% and 80%.

Required Documents For A Commercial Mortgage

- Financial Statements: Profit and loss statements, balance sheets, and cash flow statements for the past 3-5 years.

- Tax Returns: Business and personal tax returns for the past 2-3 years.

- Business Plan: Comprehensive plan detailing the business’s strategy, market, and financial projections.

- Property Information: Appraisal reports, purchase agreements, and property details.

- Personal Financial Statements: For all owners with significant stakes in the business.

Tips For Preperation

- Organize Early: Start gathering documents well in advance of the loan application.

- Accuracy: Ensure all information is accurate and up-to-date.

- Professional Assistance: Consider hiring an accountant or financial advisor to help prepare and review documents.